-

What's new

- All What's new

-

European

- What's new - All

- <hr>

- What's new - last 24 hrs

- What's new - last 7 days

- What's new - last 30 days

- <hr>

- New EU Legislation

- European Commission

- European Banking Authority

- European Securities and Markets Authority

- European Insurance and Occupational Pensions Authority

- <hr>

- Consultations and similar

- Commentaries

- <hr>

- Downloads and Exports

- Latest news by Topics

-

International

- What's new - All

- <hr>

- What's new - last 24 hrs

- What's new - last 7 days

- What's new - last 30 days

- <hr>

- Bank for International Settlements

- Basel Committee on Banking Supervision

- Egmont Group

- International Association of Insurance Supervisors

- International Monetary Fund

- <hr>

- Consultations and similar

- Commentaries

- <hr>

- Downloads and Exports

- Latest news by Topics

- Downloads and Exports

- Legislation

- Organisations

-

Commentaries

- Consultations

- Sanctioned regimes

- IFRSs

- Regulatory calendar

- Quicklinks

-

More

Table of Contents

Document Overview

AI Disclaimer

Please note that AI-generated content should not be considered legal advice. Users are encouraged to consult with qualified professionals or legal advisors where specific legal guidance is required.

We are committed to transparency and responsible use of AI in a way that supports, but never replaces, human expertise.

If you have any questions or concerns about the use of AI on our platform, please feel free to contact us.

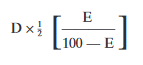

2. Amendment of section 45 (distributions) of Finance Act, 1980.

Section 45 of the Finance Act, 1980, is hereby amended by the insertion after subsection (3) of the following proviso to that subsection:

"Provided that where, as respects an accounting period, corporation tax payable by a company is, by virtue of subsection (9) (inserted by section 1 of the Finance (No. 2) Act, 1992) of section 41, reduced by the revised relief (within the meaning of the said subsection (9)), the tax credit in respect of a distribution treated for the purposes of this section as made for the accounting period shall be an amount determined by the formula -

D is the amount or value of the distribution, and

E is an amount determined by the formula -

T

_× 100

I

where -

T is the corporation tax payable by the company for the accounting period, so far as it is referable to income from the sale of those goods (within the meaning of section 41), after deducting from that tax such amount as falls to be deducted under the said section 41, and

I is the said income from the sale of those goods.".