-

What's new

- All What's new

-

European

- What's new - All

- <hr>

- What's new - last 24 hrs

- What's new - last 7 days

- What's new - last 30 days

- <hr>

- New EU Legislation

- European Commission

- European Banking Authority

- European Securities and Markets Authority

- European Insurance and Occupational Pensions Authority

- <hr>

- Consultations and similar

- Commentaries

- <hr>

- Downloads and Exports

- Latest news by Topics

-

International

- What's new - All

- <hr>

- What's new - last 24 hrs

- What's new - last 7 days

- What's new - last 30 days

- <hr>

- Bank for International Settlements

- Basel Committee on Banking Supervision

- Egmont Group

- International Association of Insurance Supervisors

- International Monetary Fund

- <hr>

- Consultations and similar

- Commentaries

- <hr>

- Downloads and Exports

- Latest news by Topics

- Downloads and Exports

- Legislation

- Organisations

-

Commentaries

- Consultations

- Sanctioned regimes

- IFRSs

- Regulatory calendar

- Quicklinks

-

More

Table of Contents

Page Overview

Document Overview

AI Summary of Article 279a Supervisory delta

This document outlines the methodology for calculating the supervisory delta for options, specifying distinct formulas based on the nature of the options and their risk categories. Institutions must employ a comprehensive approach, accounting for spot or forward prices, strike prices, volatility, and time to expiry, in line with stipulated regulatory standards.

Furthermore, the European Banking Authority (EBA) is tasked with developing draft regulatory technical standards by July 2025, aimed at refining the calculation frameworks for options related to interest rate and commodity risk, as well as clarifying positions in primary risk drivers, ensuring compliance with evolving market conditions.

AI Disclaimer

Please note that AI-generated content should not be considered legal advice. Users are encouraged to consult with qualified professionals or legal advisors where specific legal guidance is required.

We are committed to transparency and responsible use of AI in a way that supports, but never replaces, human expertise.

If you have any questions or concerns about the use of AI on our platform, please feel free to contact us.

Article 279a Supervisory delta

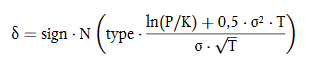

1. Institutions shall calculate the supervisory delta as follows:

(a) for call and put options that entitle the option buyer to purchase or sell an underlying instrument at a positive price on a single or multiple dates in the future, except where those options are mapped to the interest rate risk or commodity risk category, institutions shall use the following formula:

where:

δ = the supervisory delta;

sign = – 1 where the transaction is a sold call option or a bought put option;

sign = + 1 where the transaction is a bought call option or sold put option;

type = – 1 where the transaction is a put option;

type = + 1 where the transaction is a call option;

N(x) = the cumulative distribution function for a standard normal random variable meaning the probability that a normal random variable with mean zero and variance of one is less than or equal to x;

P = the spot or forward price of the underlying instrument of the option; for options the cash flows of which depend on an average value of the price of the underlying instrument, P shall be equal to the average value at the calculation date;

K = the strike price of the option;