AI Summary of Article 132c Treatment of off-balance-sheet exposures to CIUs

Institutions are required to assess the risk-weighted exposure amount for off-balance-sheet items potentially convertible into units or shares in a Collective Investment Undertaking (CIU) by applying specified risk weights. Exposure values must be calculated according to regulatory guidelines, considering approaches under relevant articles.

For minimum value commitments linked to CIUs, institutions should compute exposure values as the discounted present value of guaranteed amounts. This applies when certain conditions are met, including the obligation to pay only when market values fall below set thresholds and ensuring that retail clients are the ultimate beneficiaries. Compliance with these parameters is critical for effective risk management.

Article 132c Treatment of off-balance-sheet exposures to CIUs

1. Institutions shall calculate the risk-weighted exposure amount for their off-balance-sheet items with the potential to be converted into exposures in the form of units or shares in a CIU by multiplying the exposure values of those exposures calculated in accordance with Article 111, with the following risk weight:

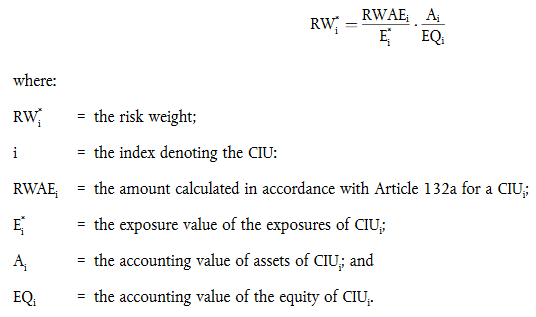

(a) for all exposures for which institutions use one of the approaches set out in Article 132a: