-

What's new

- All What's new

-

European

- What's new - All

- <hr>

- What's new - last 24 hrs

- What's new - last 7 days

- What's new - last 30 days

- <hr>

- New EU Legislation

- European Commission

- European Banking Authority

- European Securities and Markets Authority

- European Insurance and Occupational Pensions Authority

- <hr>

- Consultations and similar

- Commentaries

- <hr>

- Downloads and Exports

- Latest news by Topics

-

International

- What's new - All

- <hr>

- What's new - last 24 hrs

- What's new - last 7 days

- What's new - last 30 days

- <hr>

- Bank for International Settlements

- Basel Committee on Banking Supervision

- Egmont Group

- International Association of Insurance Supervisors

- International Monetary Fund

- <hr>

- Consultations and similar

- Commentaries

- <hr>

- Downloads and Exports

- Latest news by Topics

- Downloads and Exports

- Legislation

- Organisations

-

Commentaries

- Consultations

- Sanctioned regimes

- IFRSs

- Regulatory calendar

- Quicklinks

-

More

Table of Contents

Page Overview

Document Overview

AI Summary of Article 325bb Expected shortfall risk measure

This document outlines the methodology for calculating the expected shortfall risk measure for trading and non-trading book positions subject to foreign exchange or commodity risk. Institutions must compute this measure based on specified risk factors, incorporating both unconstrained and partial expected shortfall measures in accordance with established articles.

Furthermore, the document stipulates conditions under which institutions may reduce the frequency of these calculations from daily to weekly, provided they can demonstrate compliance with market risk assessment requirements as dictated by their competent authority.

AI Disclaimer

Please note that AI-generated content should not be considered legal advice. Users are encouraged to consult with qualified professionals or legal advisors where specific legal guidance is required.

We are committed to transparency and responsible use of AI in a way that supports, but never replaces, human expertise.

If you have any questions or concerns about the use of AI on our platform, please feel free to contact us.

Article 325bb Expected shortfall risk measure

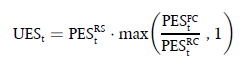

1. Institutions shall calculate the expected shortfall risk measure referred to in point (a) of Article 325ba(1) for any given date 't' and for any given portfolio of trading book positions and non-trading book positions that are subject to foreign exchange or commodity risk as follows:

ESt = the expected shortfall risk measure;

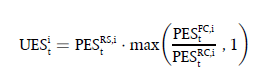

i = the index that denotes the five broad categories of risk factors listed in the first column of Table 2 of Article 325bd;

UESt = the unconstrained expected shortfall measure calculated as follows:

UESit = the unconstrained expected shortfall measure for broad risk factor category i and calculated as follows:

ρ = the supervisory correlation factor across broad categories of risk; ρ = 50 %;

= the partial expected shortfall measure that shall be calculated for all the positions in the portfolio in accordance with Article 325bc(2);

= the partial expected shortfall measure that shall be calculated for all the positions in the portfolio in accordance with Article 325bc(2);