-

What's new

- All What's new

-

European

- What's new - All

- <hr>

- What's new - last 24 hrs

- What's new - last 7 days

- What's new - last 30 days

- <hr>

- New EU Legislation

- European Commission

- European Banking Authority

- European Securities and Markets Authority

- European Insurance and Occupational Pensions Authority

- <hr>

- Consultations and similar

- Commentaries

- <hr>

- Downloads and Exports

- Latest news by Topics

-

International

- What's new - All

- <hr>

- What's new - last 24 hrs

- What's new - last 7 days

- What's new - last 30 days

- <hr>

- Bank for International Settlements

- Basel Committee on Banking Supervision

- Egmont Group

- International Association of Insurance Supervisors

- International Monetary Fund

- <hr>

- Consultations and similar

- Commentaries

- <hr>

- Downloads and Exports

- Latest news by Topics

- Downloads and Exports

- Legislation

- Organisations

-

Commentaries

- Consultations

- Sanctioned regimes

- IFRSs

- Regulatory calendar

- Quicklinks

-

More

Table of Contents

Page Overview

Document Overview

AI Summary of Article 325af Intra bucket correlations for general interest rate risk

This document outlines the correlation parameters applicable to the weighted sensitivities of general interest rate risk factors. Within the same maturity bucket, when comparing two sensitivities linked to different curves, a high correlation of 99.90% (ρkl) is mandated. For sensitivities associated with the same curve but differing maturities, the correlation will adhere to a specified formula.

Moreover, when sensitivities from different curves and maturities are considered, the correlation is derived from the previous parameter, adjusted to 99.90%. Notably, correlation levels between interest and inflation risk factors are established at 40%, while interactions between cross-currency basis risk factors and general interest rate risks are set at 0%.

AI Disclaimer

Please note that AI-generated content should not be considered legal advice. Users are encouraged to consult with qualified professionals or legal advisors where specific legal guidance is required.

We are committed to transparency and responsible use of AI in a way that supports, but never replaces, human expertise.

If you have any questions or concerns about the use of AI on our platform, please feel free to contact us.

Article 325af Intra bucket correlations for general interest rate risk

1. Between two weighted sensitivities of general interest rate risk factors WSk and WSl within the same bucket, and with the same assigned maturity but corresponding to different curves, correlation ρkl shall be set at 99,90 %.

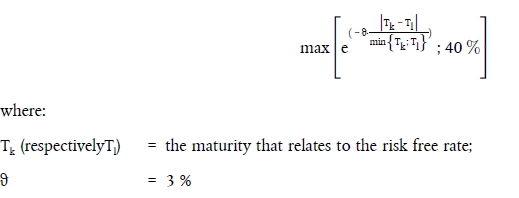

2. Between two weighted sensitivities of general interest rate risk factors WSk and WSl within the same bucket, corresponding to the same curve, but having different maturities, correlation shall be set in accordance with the following formula:

3. Between two weighted sensitivities of general interest rate risk factors WSk and WSl within the same bucket, corresponding to different curves and having different maturities, the correlation ρkl shall be equal to the correlation parameter specified in paragraph 2, multiplied by 99,90 %.

4. Between any given weighted sensitivity of general interest rate risk factors WSk and any given weighted sensitivity of inflation risk factors WSl, the correlation shall be set at 40 %.