-

What's new

- All What's new

-

European

- What's new - All

- <hr>

- What's new - last 24 hrs

- What's new - last 7 days

- What's new - last 30 days

- <hr>

- New EU Legislation

- European Commission

- European Banking Authority

- European Securities and Markets Authority

- European Insurance and Occupational Pensions Authority

- <hr>

- Consultations and similar

- Commentaries

- <hr>

- Downloads and Exports

- Latest news by Topics

-

International

- What's new - All

- <hr>

- What's new - last 24 hrs

- What's new - last 7 days

- What's new - last 30 days

- <hr>

- Bank for International Settlements

- Basel Committee on Banking Supervision

- Egmont Group

- International Association of Insurance Supervisors

- International Monetary Fund

- <hr>

- Consultations and similar

- Commentaries

- <hr>

- Downloads and Exports

- Latest news by Topics

- Downloads and Exports

- Legislation

- Organisations

-

Commentaries

- Consultations

- Sanctioned regimes

- IFRSs

- Regulatory calendar

- Quicklinks

-

More

Table of Contents

Page Overview

Document Overview

AI Summary of Article 226 Scaling up of volatility adjustment under the Financial Collateral Comprehensive Method

The volatility adjustments mandated in Article 224 are critical for institutions conducting daily revaluations. When revaluations occur less frequently than daily, institutions are required to implement larger volatility adjustments. This scaling must be conducted using the square-root-of-time formula, which ensures that the adjustments remain proportional to the risks associated with the revaluation period.

Under this framework, the volatility adjustment (H) is determined by the daily revaluation value (HM) and is scaled according to the actual number of business days (NR) between revaluations, relative to the specified liquidation period (TM) for the transaction type. Adherence to these guidelines is essential for maintaining compliance and mitigating financial risk.

AI Disclaimer

Please note that AI-generated content should not be considered legal advice. Users are encouraged to consult with qualified professionals or legal advisors where specific legal guidance is required.

We are committed to transparency and responsible use of AI in a way that supports, but never replaces, human expertise.

If you have any questions or concerns about the use of AI on our platform, please feel free to contact us.

Article 226 Scaling up of volatility adjustment under the Financial Collateral Comprehensive Method

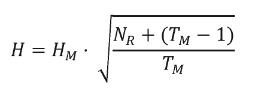

The volatility adjustments set out in Article 224 are the volatility adjustments an institution shall apply where there is daily revaluation. Where the frequency of revaluation is less than daily, institutions shall apply larger volatility adjustments. Institutions shall calculate them by scaling up the daily revaluation volatility adjustments, using the following square-root-of-time formula:

where:

H = the volatility adjustment to be applied;

HM = the voatility adjustment where there is daily revaluation;

NR = the actual number of business days between revaluations;

TM = the liquidation period for the type of transaction in question.