AI Summary of Article 162 Maturity

Maturity (M) defaults to 2.5 years where an institution has not been authorised to use its own LGD estimates, except 0.5 years for securities financing transactions, or may be calculated as provided. Where an institution applies its own LGD estimates, M is expressed in years, subject to paragraphs 3–5, and capped at five years except as provided in Article 384(2). Calculation methods include: (a) a cash-flow weighted formula using contractually payable CFt; (b) derivatives under master netting using a notional-weighted average maturity, minimum one year; (c) fully/nearly-fully collateralised derivatives and margin lending under netting, weighted average, minimum ten days; (d) repo/securities/commodities lending under netting, weighted average, minimum five days; (da) secured lending under netting, weighted average, minimum twenty days; (db) mixed sets use the longest applicable holding period (ten or twenty days); (e) purchased receivables with PD permission use exposure-weighted average maturity (drawn) and special rules for undrawn amounts, minimum ninety days; (f) otherwise M equals the maximum permitted remaining time to discharge obligations, minimum one year; (j) revolving exposures use the facility’s maximum contractual termination date.

For IMM exposures with a longest-dated contract over one year, M is calculated by a specified formula incorporating a one-year dummy, expected and effective expected exposures and discount factors. An internal model for one-sided CVA may, with permission, use the model’s effective credit duration as M. If all contracts in a netting set had original maturities below one year, the cash-flow formula applies. For CVA approaches under Article 382a(1), M is capped at one in the Article 153(1)(iii) formula for corresponding counterparty risk RWEAs. Where documentation mandates daily re-margining and revaluation and permits prompt collateral liquidation or set-off, M is the notional-weighted average remaining maturity with a minimum of one day for specified collateralised transactions and qualifying short‑term exposures (FX settlement, self‑liquidating short‑term trade finance and corporate receivables ≤1 year, usual securities settlement periods, short cash payment settlements and short confirmed/issued letters of credit). Institutions may elect paragraph 1 M for Union corporates that are not large corporates; maturity mismatches follow Chapter 4; days are converted to years by dividing by 365.25.

Article 162 Maturity

1. For exposures for which an institution has not received permission from the competent authority to use own estimates of LGD, the maturity value (M) shall be applied consistently and, either be set at 2,5 years, except for exposures arising from securities financing transactions, for which M shall be 0,5 years, or, alternatively, be calculated in accordance with paragraph 2.

2. For exposures for which an institution applies own estimates of LGD, the maturity value (M) shall be calculated using periods expressed in years, as set out in this paragraph and subject to paragraphs 3, 4 and 5 of this Article. M shall be no greater than five years, except in the cases specified in Article 384(2) where M as specified therein shall be used. M shall be calculated as follows in each of the following cases:

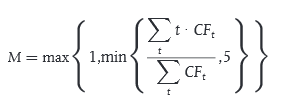

(a) for an instrument subject to a cash flow schedule, M shall be calculated in accordance with the following formula:

where CFt denotes the cash flows (principal, interest payments and fees) contractually payable by the obligor in period t;